The economics of decarbonizing fleets are demonstrably viable. Now commercial transport operators need to identify the best way to capture value. McKinsey reports about it based on US data.

These segment-specific dynamics are reflected in McKinsey’s financial projections. On a TCO basis, light-commercial vehicles LCVs are already “in the money,” and they expect medium-duty trucks (MDT) to deliver TCO parity with ICE alternatives in 2024. heavy-duty trucks (HDTs) will achieve parity toward the middle of the decade, accelerated by tax incentives for new MDTs and HDTs.

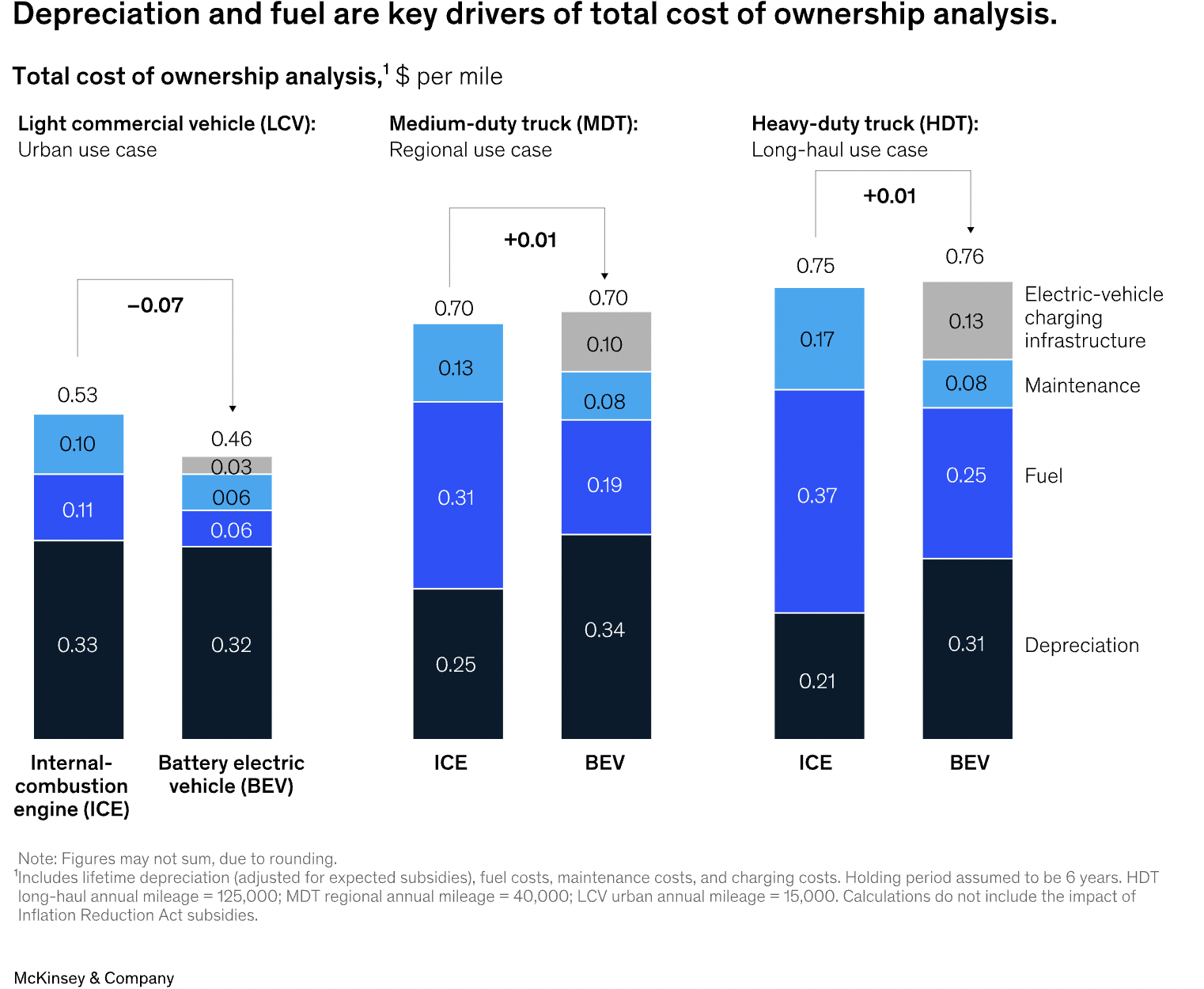

However, the most prominent components of TCO differential across fleet subsegments are likely to include depreciation (net of asset price, subsidies, and residual value), fueling, maintenance (BEV battery and motor), and the fixed and operating costs of charging infrastructure. Across all vehicle classes, new BEVs are more expensive than ICE vehicles. However, this is offset by tax incentives and stronger residuals.

By 2025, factors including lower depreciation, fuel costs, and maintenance costs for LCV BEV will more than offset incremental charging infrastructure costs. MDT BEV will offer a TCO equivalent to its ICE counterparts: higher depreciation and charging infrastructure costs will be balanced by savings on fuel and maintenance. In the HDT segment, depreciation costs will mean the TCO will be about 10 percent higher than the ICE equivalents.

Given the current uncertainty affecting energy markets, fleet operators will sensibly insert contingencies for price volatility into their calculations. As a rule of thumb, a 50 percent increase in the price of diesel, electricity, or hydrogen would lead to an overall TCO increase of 10 to 20 percent, even in the most fuel-intensive use cases. According to McKinsey, electricity’s resilience to price fluctuations is a factor in its favor.

Other constraints include the significant cash outflows and time required to purchase vehicles, upgrade warehouses and hubs, obtain permits, and coordinate with utilities, particularly for smaller businesses. In addition, operators may be concerned that driver productivity may decline, at least initially, with longer shifts necessary to incorporate charging before route optimization is refined and charging speeds increase.

Operators have concerns over peak-demand fees in electricity markets, which may increase costs as they strive to balance scheduling and charging needs. Suboptimal charging practices can also impact BEV residual values because battery quality and life span will degrade over time. Additionally, training will be required for maintenance staff, adding another cost to the transition process.

For operators owning a range of vehicle types, a more nuanced calculation of TCO benefit will be required. In any calculation, companies must make judgments that reflect their specific circumstances.

Source: McKinsey