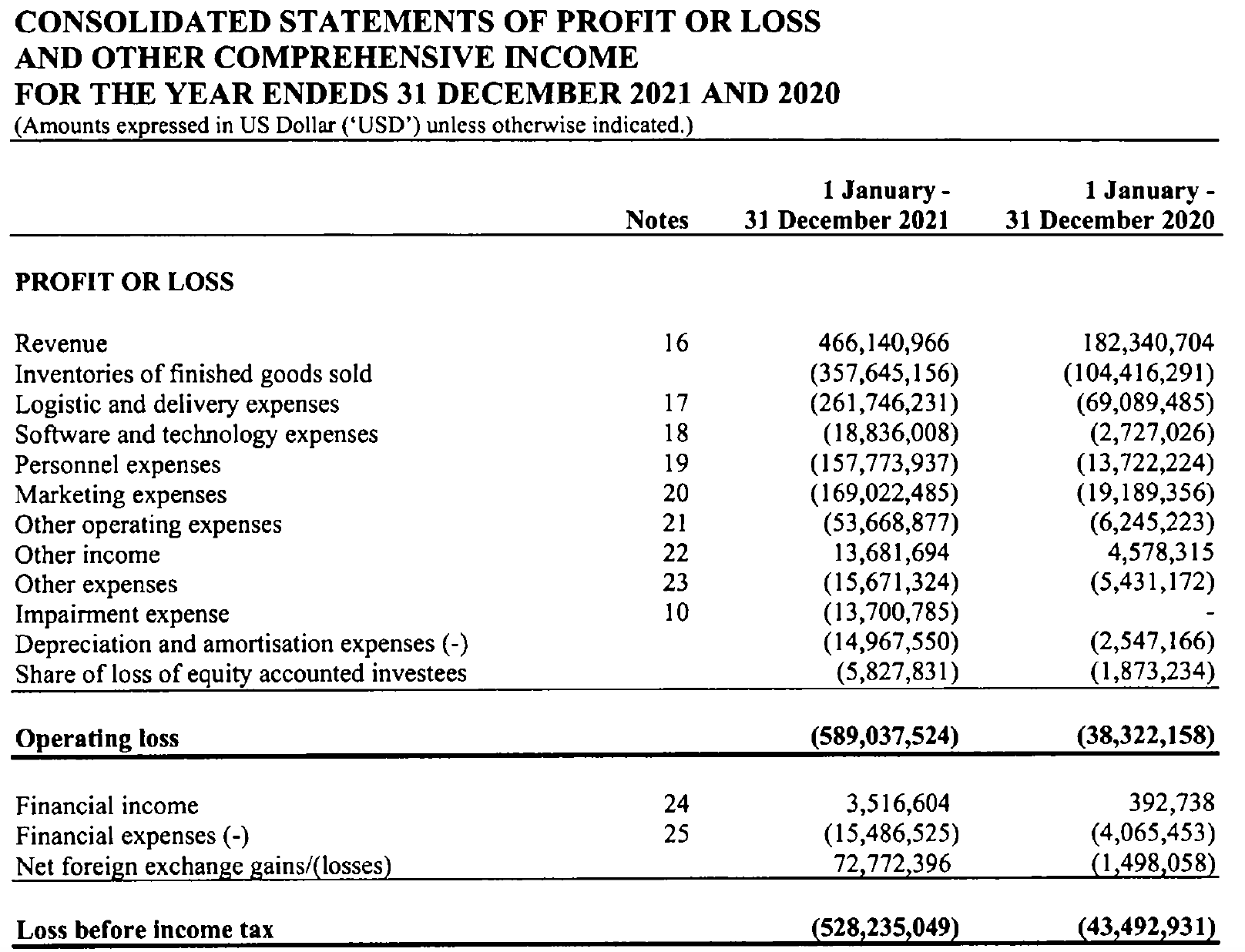

Getir lost almost $600 mln in 2021 on a European revenue of $466 mln in 2021. Nevertheless, Getir has enough cash on hand to last for a while. At the end of 2021, the company had $547 mln in cash on its balance sheet, and in March 2022, it raised another $768 mln in fresh capital from a group of investors (valued at $12 bln in March 2022).

Financial data 2021

Getir published its 111-page annual financial report on the website of the Chamber of Commerce. This is an exciting document for everybody who wants a closer look at the financial background of quick commerce (q-commerce).

The fulfillment cost was a whopping 56% of revenue in 2021. The gross margin (revenue versus the cost of goods sold) was 23%. Marketing expenses were 36% of revenue. Inventory levels were around two months. In 2021 Getir invested $35 mln in the Netherlands market alone.

Is there a road to profit in q-commerce?

To understand the changes taking place in the q-commerce market, Roland Berger recently surveyed more than 6,000 consumers in Germany, France, and the United Kingdom. Using this data, Roland Berger analyzed the potential of q-commerce and looked at how omnichannel retailers can rise to the challenge.

Overall, 46 percent of respondents said they would switch more of their shopping to q-commerce. This was against a background of rising fears about a looming recession. In more normal times, respondents might have been even more enthusiastic about embracing q-commerce.

Price, product availability, and delivery fees are key for q-commerce. But other factors, such as customer experience, fast delivery, and product quality, are almost as important.

The size of the market

The q-commerce market initially focused primarily on groceries and meal deliveries. Now, players have started expanding into other retail categories, for example, offering a cross-category assortment of fashion, beauty, and home decoration items.

The potential market size means that retailers would be wrong to ignore it. For example, if around 12 percent of the EUR 730 billion groceries market in the United Kingdom, France, and Germany move online by 2030 and q-commerce accounts for just 15 percent of online orders, the market will be worth EUR 13 billion.

If q-commerce expands to include more online product categories, this would mean a sizeable additional increase in market size. According to Roland Berger, the critical question is whether the revenues from product margins, commission fees, customer delivery fees, service fees, and in-app advertisements can cover operating costs and make the business model lucrative. The answer to that question is yet unclear.

Product prices in q-commerce are similar to those in the supermarket, marketing for brand-building can account for up to 30 percent of total costs in the initial phase (as is with Getir at 36%), and delivery fees rarely cover the actual costs (as is with Getir at 56%), according to Roland Berger. Is there a road to profit in q-commerce? Maybe not… but it will take endurance and deep pockets.

Overall, Roland Bergers believes that the share of q-commerce will grow but will eventually hit the ceiling, as shoppers only need certain items immediately. Growth will come not only at the expense of other e-commerce and convenience stores but also from new demands previously unmet – such as more snacks during movie night.

The number of new market entrants means that competitive pressure is high, as witnessed by the massive advertising and marketing levels. According to Roland Berger, Q-commerce players must strive to outperform their competitors.

Achieving sustainable profitability

The key challenge is how to achieve sustainable profitability. An increasingly difficult goal in the current macroeconomic climate. According to Roland Berger, to master the challenge, players can consider several top-line and bottom-line actions.

They may explore additional revenue streams to boost the top line, such as selling digital space on their apps to consumer goods companies for use in promotions, preferential product placement, and media placement. They may also consider sharing data on consumer shopping behavior or product preferences.

Q-commerce players can increase their top line by adjusting their delivery terms. For example, they could increase delivery fees, differentiating based on distance. However, consumers are highly sensitive to delivery fees. An alternative is to introduce minimum order sizes to cover transportation costs.

Dynamic pricing is an efficient way to benefit from demand in peak times. Some players have already started benchmarking their prices in advertising with brick-and-mortar retailers rather than their q-commerce competitors. Players can also optimize their assortment by adding high-margin products and considering cross-selling options, for example, through product bundles.

Increasing the price premium compared to offline prices is another effective tactic, although this will be difficult given consumers’ current price sensitivity.

To increase the bottom line, q-commerce players can look at marketing costs and discounts. These currently consume a lot of q-commerce revenues, and cutting them would significantly impact the bottom line.

Players can further improve the bottom line by introducing innovations in fulfillment operations, such as micro-fulfillment centers that add q-commerce pick capacity in existing spaces without creating large, capital-intensive automated warehouses. The more items are handled, the more efficiency improvements in picking are likely, leading to a cost reduction. Efficiency gains are also possible by optimizing last-mile delivery through better routing and higher driver utilization.

Keep growing: get big or get out

Get big or get out? Getir has recently closed its acquisition of German rival Gorillas in a deal that values the combined group at $10 bn as consolidation in the q-commerce market accelerates. The deal brings together two of Europe’s biggest beneficiaries of the pandemic’s boom in start-up financing, raising more than $3 bn from venture capitalists since 2020 to grow their services by delivering groceries and convenience-store items in as little as 10 minutes.

Getir, US GoPuff, and Germany’s Flink are the last surviving big players in the sector. “Markets go up and down, but consumers love our service, and convenience is here to stay,” said Nazim Salur, founder of Getir, in a statement about the deal. “The super-fast grocery delivery industry will steadily grow for many years to come, and Getir will lead this category it created seven years ago.”

Source of figures: Roland Berger.

This is very interesting information, many thanks for publishing. However, it seems that the annual report for Getir BV is no longer available from the Chamber of Commerce website (after I created an account and logged in).

Could you please check if that’s also the same for you?

Also, which countries does Getir BV operate in? It looks like Europe, excluding Turkey – is that right.

Look forward to your reply, many thanks and Happy Holidays!