It’s easy to envision self-driving trucks safely and efficiently carrying shipments down highways. But that’s only part of any product’s journey between manufacturers and customers. How will the new mobility ecosystem handle the whole trip, including last-mile delivery?

A Deloitte study on last-mile delivery presents a four-state model for rethinking and redesigning last-mile delivery.

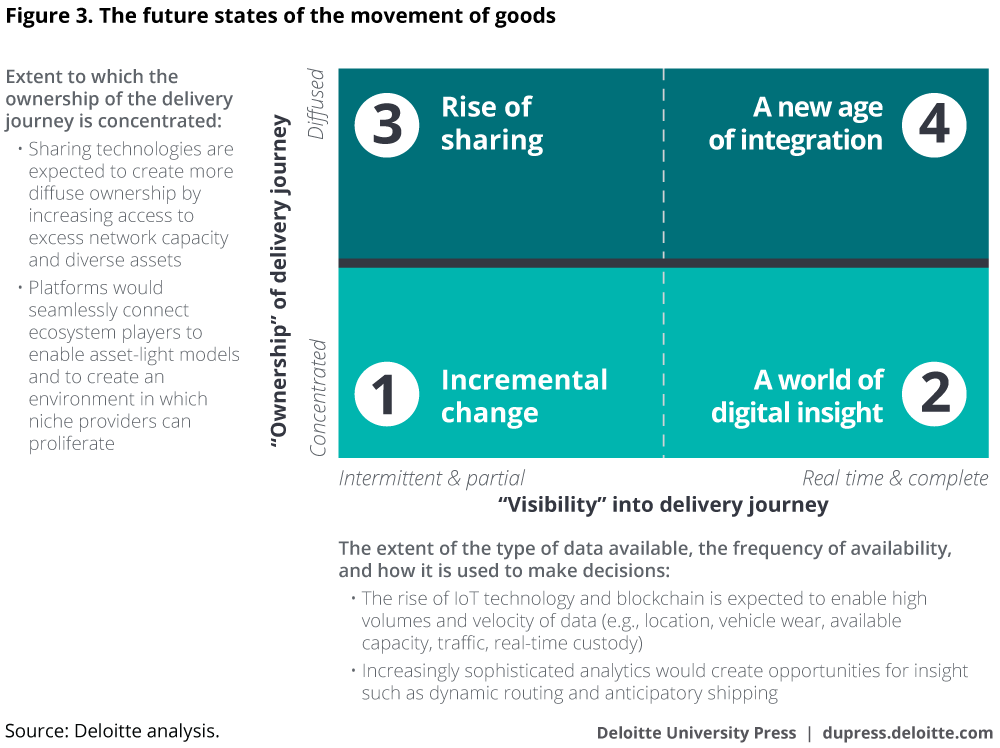

State 1: Incremental change

Customer expectations around shipping continue to rise, but inefficiencies within the ecosystem make meeting those expectations challenging. Ecosystem players use third-party assets to augment their fleets, but transactional frictions remain. Players sign contracts far in advance to ensure access to third-party assets or rely on human brokers to manually find extra capacity in the marketplace.

Platforms continue to emerge, but the challenge of integrating them into the business persists. Ultimately, these frictions result in excess capacity remaining in the transportation network and limit the integration of niche offerings into the supply chain.

Varied deployment of telematics and connected vehicle technologies inform owners and operators about the status of their own fleets, but the availability of data about the ecosystem as a whole is limited. Many processes remain paper-based. Analytics are largely descriptive and rely on humans for interpretation and decision making. With limited data and analytical capability, inefficiencies in the transportation network abound.

State 2: A world of digital insight

Increasingly prevalent deployment of telematics and IoT technology generates a significant volume of data about the fleet. Processes are no longer paper documents based but reside in the cloud, expanding the digital data set. The most forward-thinking carriers and retailers continue to build their digital capabilities.

Companies have real-time insight into their own supply chains, which improves accuracy and permits more efficient use of capacity. Predictive analytics help them better manage inventory by type and location. Analytics change the cost equation, allowing businesses to create price differentials that they can pass to customers as savings. However, the last mile remains strained because excess capacity is not shared, so local optimization, as opposed to ecosystem-wide optimization, remains the norm.

State 3: Rise of sharing

Sharing platforms become increasingly relevant and an integral part of the ecosystem, even more important than human brokers and typical contractual arrangements. These platforms reduce switching costs and drive a proliferation of third party shipping options, making the last mile of delivery extremely fragmented. This complexity is offset by increased vehicle utilization, which reduces the cost per delivery. Platforms make integrating additional shipping options such as light electric vehicles, delivery robots, drones, and smart lockers easier for businesses, helping to meet ever-rising customer expectations.

A few platforms emerge as the dominant players in the market and effectively coordinate the fragmented last mile. Larger, integrated players compete against the dominant platforms on price and service level. With data as the new currency, there is limited sharing between the dominant platforms and the larger, integrated players, leaving inefficiency in the ecosystem.

State 4: A new age of integration

The creation of digital markets for the movement of goods enables shipments to be delivered at the right place at the right time by the right method, resulting in lower costs and greater convenience across the ecosystem. These markets are made more efficient by integrating and distributing data flows from multiple sources, giving customers and shippers constant real-time access to the location and status of their goods and assets. Smart, mobile lockers dynamically move throughout a city, all linked by a digital platform that any in-network carrier can securely access.

Carriers and retailers routinely and easily source third-party providers for the last mile, reducing both the cost and speed of delivery. Carriers and retailers that can place themselves at the center of this digital ecosystem are the ones likely to thrive. While we expect consolidation among the players at the center of the ecosystem, a host of niche providers and informal, part-time couriers will likely proliferate, seizing last-mile market share.

Source: Deloitte