Online grocery in Europe is returning to growth and is increasingly evolving into an independent, profitable format with a differentiated value proposition. Online grocery lost market share in 2023, but consumers are starting to return as spending power recovers, says McKinsey. The net intent of consumers to buy more food online has returned to positive, increasing by eight percentage points in the first quarter of 2024.

McKinsey expects e-grocery in Europe to grow faster than the grocery market over the next years. Restaurant meal delivery might also grow faster than e-grocery. Pure players, in particular, show extraordinary growth rates as they expand into new regions. For instance, Picnic grew more than 30 percent per annum over the past five years, driven by rapid expansion.

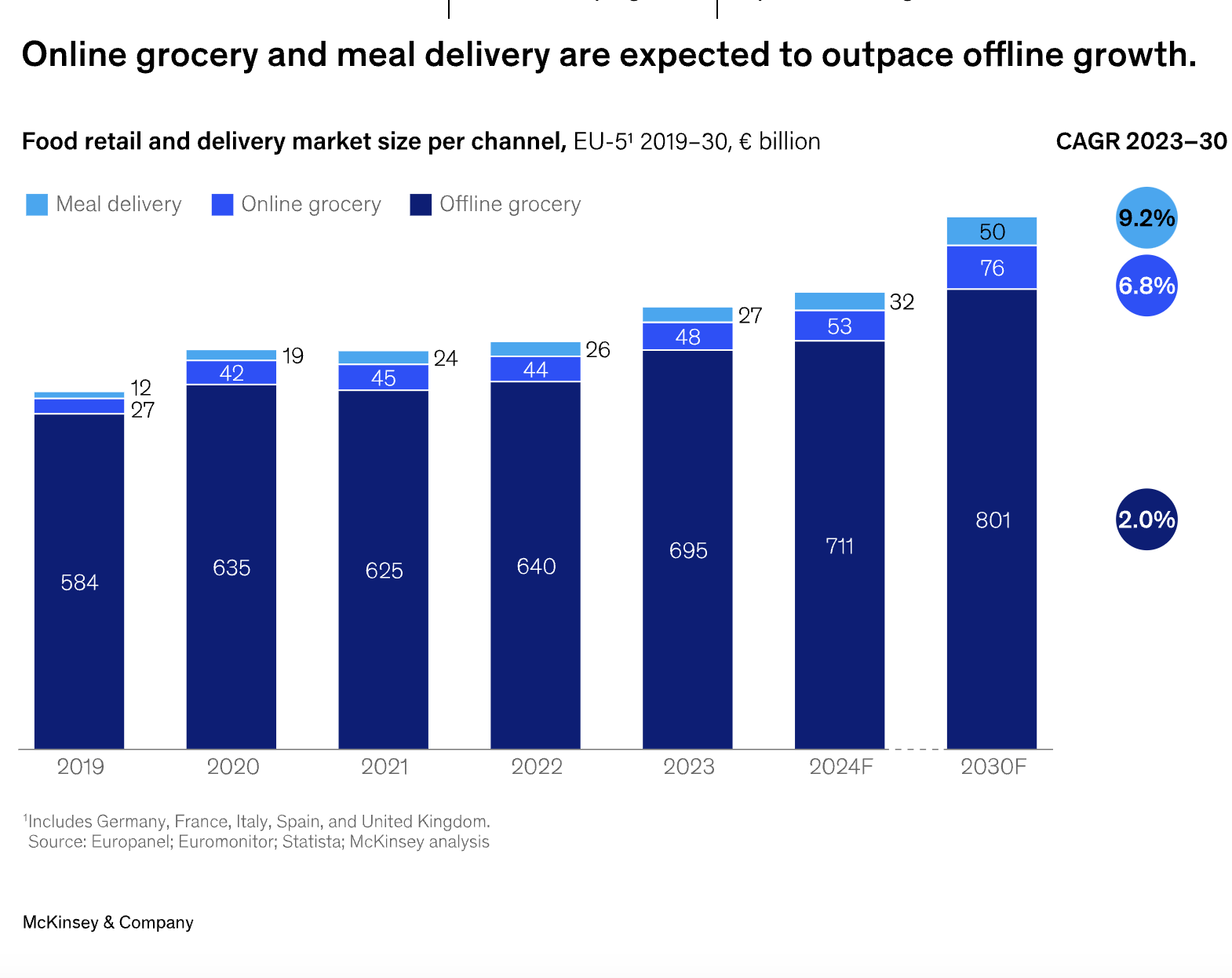

Figure: McKinsey

Pure players are starting to reach profitability

Pure players are starting to reach profitability. For instance, Rohlik is profitable. Picnic claims to be “operationally profitable in mature markets,” Ocado returned to profitability in 2023. Moreover, leading meal delivery players have also reached breakeven (DoorDash and Deliveroo throughout 2023), thanks to a successful shift of priorities from growth to rightsizing.

Increasingly, consumers expect different value propositions from online and offline channels. It is becoming progressively clear that the two channels satisfy different shopping needs. For example, 37 percent of consumers in our UK survey (two percentage points higher than in 2023) always shop at a different banner online than offline because they exhibit different needs by channel. In addition, UK consumers see promotions as more important than price for offline store selection, while for online, price is more important than promotions.

Source: McKinsey