The Global EV Outlook is an annual publication that identifies and assesses recent developments in electric mobility worldwide. It is developed with the support of members of the Electric Vehicles Initiative (EVI).

Combining analysis of historical data with projections – now extended to 2035 – the report examines key areas of interest, such as the deployment of electric vehicles and charging infrastructure, battery demand, investment trends, and related policy developments in major and emerging markets. It also considers wider EV adoption for electricity and oil consumption and greenhouse gas emissions. The report includes an analysis of lessons learned from leading markets, providing information for policymakers and stakeholders on policy frameworks and market systems that support electric vehicle uptake.

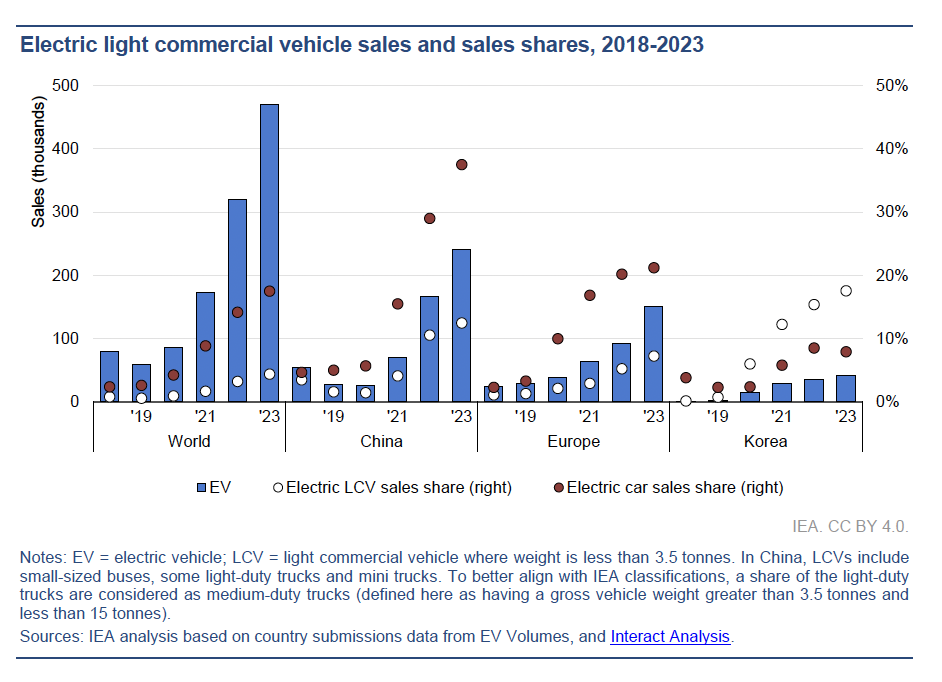

Electric light commercial vehicles

Electric light commercial vehicles (LCVs) saw a notable uptick in sales in 2023, with one in twenty-five LCVs sold globally being electric, mirroring the trajectory of electric passenger cars. This surge in demand for electric LCVs was evident as global sales soared by over 50%, pushing the market share to nearly 5%.

China and Europe emerged as prominent markets for electric LCVs, witnessing substantial growth in sales. In China, electric LCV sales surpassed 240,000 units, while Europe experienced a 60% surge, reaching almost 150,000 units. This surge was part of a broader trend of increasing sales of electric and traditional internal combustion engine (ICE) LCVs.

As the electric LCV market matures, numerous original equipment manufacturers (OEMs) have unveiled new electric models and formed strategic partnerships. Some of these models cater to specific commercial niches, like the B-ON Pelkan electric delivery van. In collaboration with Uber, Kia introduced a modular van design adaptable to various commercial tasks, from shuttling to last-mile delivery.

The average range of new LCVs increased by 55% from 2015 to 2023. Notably, models such as the Hyundai Porter and Ford E-Transit showcased significantly longer ranges, ranging from 210 to 260 km, compared to around 170 km for popular models like the Nissan e-NV200 and Renault Kangoo BEV in 2015. Despite this progress, companies expanding their electric fleets emphasize the need for improved accuracy in range labeling.

South Korea stands out as a market where electric LCV penetration outpaces that of electric passenger cars. The Hyundai Porter and Kia Bongo are the sole electric LCV models available in the country. They suit the Korean light freight market well with their suitability for shorter distances. Moreover, these models offer favorable pricing compared to ICE equivalents.

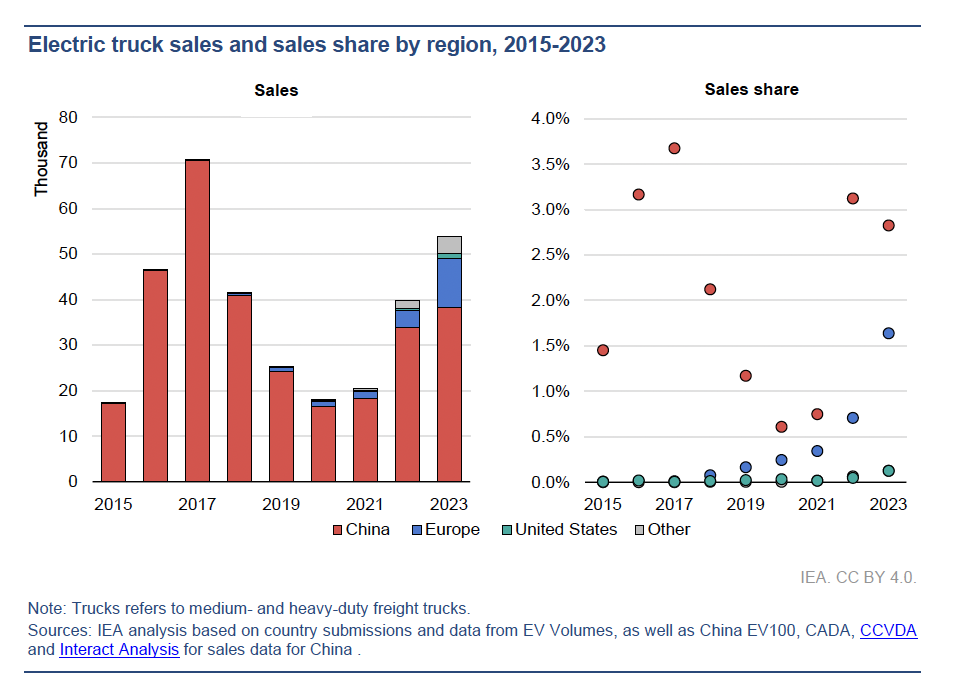

Electric trucks

In 2023, sales of electric trucks surged by 35% compared to 2022, surpassing electric bus sales for the first time with approximately 54,000 units sold globally. China emerged as the dominant market for electric trucks, comprising 70% of global sales, although this share decreased from 85% in 2022. Europe witnessed a nearly threefold increase in electric truck sales, exceeding 10,000 units, equating to a sales share of over 1.5%. Meanwhile, the United States also experienced a threefold increase, reaching only 1,200 units, accounting for less than 0.1% of total truck sales.

Expectations suggest that the upward trend in electric truck sales will persist, driven by robust policies such as the European Union’s CO2 standards for Heavy-Duty Vehicles (HDVs), aiming for a 90% reduction in CO2 emissions by 2040. Similarly, the United States anticipates up to 60% ZEV sales shares by 2032 across various segments, propelled by newly adopted heavy-duty emissions regulations.

At the municipal level, initiatives like zero-emission zones for freight are being implemented in 15 diverse cities worldwide, encompassing locations such as London, Los Angeles, Madrid, and Shenzhen. These efforts, collectively impacting over 52 million people, aim to promote sustainable freight transport. Organizations like EV100+, the Global Memorandum of Understanding on Zero-Emission Medium and Heavy-Duty Vehicles, and various coalitions advocate for ambitious policies, accelerated sales targets, and zero-emission government fleets.

In the United States, demonstration projects are underway to identify segments ripe for electrification. The Run on Less – Electric DEPOT initiative, launched in June 2023 by the North American Council for Freight Efficiency and the Rocky Mountain Institute, deployed nearly 300 electric trucks to gather data on viability and challenges in electric truck usage.

Similarly, the UK Government’s USD 250 million investment in the Zero Emission HGV and Infrastructure Programme aims to conduct real-world trials of zero-emission trucks. This program will deploy 370 trucks and establish nearly 60 refueling and electric charging sites.

Outside of China, electric truck adoption is gaining traction in Emerging Markets and Developing Economies (EMDEs). In India, the Electric Freight Accelerator for Sustainable Transport, launched by NITI Aayog, has catalyzed collaboration between the government and private sector partners to promote large-scale freight electrification. Sixteen major manufacturing and logistics companies have expressed demand for 7,750 electric freight vehicles by 2030, necessitating focused efforts on policy regulation, market certainty, pilot support, infrastructure development, and financing platforms to attract private investments.

Chinese OEMs lead the pack in producing the highest number of battery electric Heavy-Duty Vehicles (HDVs), totaling 430 models, with a notable focus on buses suitable for urban public transport, comprising nearly 40% of all models. In 2021, Chinese OEMs introduced nearly 150 bus models alone, significantly expanding options in the world’s largest electric bus market.

In contrast, North American OEMs produce a smaller range of battery electric models, numbering over 170, with a predominant focus on the medium-duty truck market, constituting over 60% of all models. Emerging brands like Rizon are targeting the electric medium-duty segment in North America, where electric trucks are increasingly competitive with diesel counterparts in terms of total cost of ownership, particularly when charged at depots.

Despite fewer battery-electric models, European OEMs present a more evenly distributed range across segments, offering approximately 120 models. They boast the highest share of heavy-duty trucks, with over 20% of all models. This has enabled European OEMs, notably the Volvo group, to secure a significant portion of the European and North American heavy-duty electric truck markets. Additionally, European OEMs manufacture many niche vehicles like refuse trucks, which are already cost-competitive with internal combustion engine counterparts.

On average, individual Chinese OEMs produce a wider variety of models across segments compared to their counterparts in North America and Europe. Roughly half of Chinese OEMs manufacture models for a single segment, contrasting with around 70% in North America and Europe.

Source: Global EV Outlook